Butterfly Spread Strategy: What It Is and How It Works

A butterfly spread is a defined-risk, neutral multi-leg options strategy that profits when the underlying asset closes at or near a specific price at expiration. It combines elements of both credit and debit spreads into a single position, creating a narrow profit zone with capped risk on both sides. This article covers how the butterfly spread works, how to calculate its max profit, max loss, breakevens, and when traders use it.

What Is a Butterfly Spread?

A long butterfly spread is a defined-risk, neutral options strategy built around three strike prices. The trade profits when the underlying lands near the short strike price at expiration. Your max loss and max profit are both locked in the moment you enter the position.

You can build a butterfly with calls or puts, and it can be structured as a debit or a credit. The core architecture is the long butterfly spread variant: buy one option at a lower strike, sell two at a middle strike, and buy one at a higher strike—all with the same option type (all calls or all puts). The wings are typically equidistant from the body to ensure that the debit spread and credit spread portions of the trade are equal widths, which ensures the max loss is the debit paid up front.

.png?format=png&auto=webp&quality=90&width=1000&disable=upscale)

How the Butterfly Spread Is Built

The long call butterfly is a common version of the strategy. Here is how the legs typical break down:

Leg | Action | Strike | What It Does |

|---|---|---|---|

Lower wing | Buy 1 call | ITM | Sets the lower bound of defined risk |

Body | Sell 2 calls | At or near ATM | Collects premium, defines the max profit zone |

Upper wing | Buy 1 call | OTM | Sets the upper bound of defined risk |

Leg | Action |

|---|---|

Lower wing | Buy 1 call |

Body | Sell 2 calls |

Upper wing | Buy 1 call |

Leg | Strike |

|---|---|

Lower wing | ITM |

Body | At or near ATM |

Upper wing | OTM |

Leg | What It Does |

|---|---|

Lower wing | Sets the lower bound of defined risk |

Body | Collects premium, defines the max profit zone |

Upper wing | Sets the upper bound of defined risk |

A long put butterfly follows a similar structure using puts instead of calls.

Leg | Action | Strike | What It Does |

|---|---|---|---|

Lower wing | Buy 1 put | ITM | Sets the lower bound of defined risk |

Body | Sell 2 puts | At or near ATM | Collects premium, defines the max profit zone |

Upper wing | Buy 1 put | OTM | Sets the upper bound of defined risk |

Leg | Action |

|---|---|

Lower wing | Buy 1 put |

Body | Sell 2 puts |

Upper wing | Buy 1 put |

Leg | Strike |

|---|---|

Lower wing | ITM |

Body | At or near ATM |

Upper wing | OTM |

Leg | What It Does |

|---|---|

Lower wing | Sets the lower bound of defined risk |

Body | Collects premium, defines the max profit zone |

Upper wing | Sets the upper bound of defined risk |

The iron butterfly swaps same-type options for a mix of calls and puts. Instead of selling two calls or puts at the body, you sell an at-the-money call and an at-the-money put simultaneously, then buy wings on each side, creating a short call spread and a short put spread. The result is a net credit rather than a debit, but the risk profile is very similar to a regular butterfly constructed with the same option type.

Leg | Action | Strike | What It Does |

|---|---|---|---|

Lower wing | Buy 1 put | ITM | Sets the lower bound of defined risk |

Body | Sell 1 put Sell 1 call | At or near ATM | Collects premium, defines the max profit zone |

Upper wing | Buy 1 call | OTM | Sets the upper bound of defined risk |

Leg | Action |

|---|---|

Lower wing | Buy 1 put |

Body | Sell 1 put Sell 1 call |

Upper wing | Buy 1 call |

Leg | Strike |

|---|---|

Lower wing | ITM |

Body | At or near ATM |

Upper wing | OTM |

Leg | What It Does |

|---|---|

Lower wing | Sets the lower bound of defined risk |

Body | Collects premium, defines the max profit zone |

Upper wing | Sets the upper bound of defined risk |

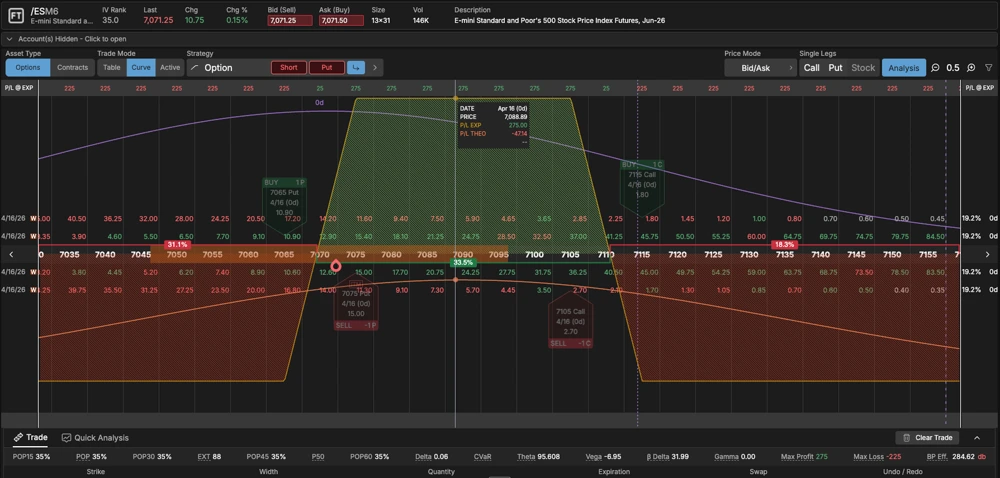

Butterfly Spread Examples

Long Call Butterfly

Say TSTY is trading at $500. Here is what a long call butterfly looks like with $10-wide wings:

Leg | Strike | Action | Premium |

|---|---|---|---|

Lower wing | $490 call | Buy 1 | -$12.00 |

Body | $500 call | Sell 2 | +$5.50 (x2) |

Upper wing | $510 call | Buy 1 | -$2.00 |

Leg | Strike |

|---|---|

Lower wing | $490 call |

Body | $500 call |

Upper wing | $510 call |

Leg | Action |

|---|---|

Lower wing | Buy 1 |

Body | Sell 2 |

Upper wing | Buy 1 |

Leg | Premium |

|---|---|

Lower wing | -$12.00 |

Body | +$5.50 (x2) |

Upper wing | -$2.00 |

Net debit: $12.00 + $2.00 - $11.00 = $3.00 per share. Total cost per spread set: $300.

Metric | Value | How It's Calculated |

|---|---|---|

Max Profit | $700 per set | Strike width between middle and lower strike ($10) minus net debit ($3.00) = $7.00 x 100 |

Max Loss | $300 per set | Net debit paid x 100 |

Lower Breakeven | $493.00 | Lower long strike + net debit ($490 + $3) |

Upper Breakeven | $507.00 | Upper long strike - net debit ($510 - $3) |

Profit Zone | $493 to $507 | The range between both breakevens |

Metric | Value |

|---|---|

Max Profit | $700 per set |

Max Loss | $300 per set |

Lower Breakeven | $493.00 |

Upper Breakeven | $507.00 |

Profit Zone | $493 to $507 |

Metric | How It's Calculated |

|---|---|

Max Profit | Strike width between middle and lower strike ($10) minus net debit ($3.00) = $7.00 x 100 |

Max Loss | Net debit paid x 100 |

Lower Breakeven | Lower long strike + net debit ($490 + $3) |

Upper Breakeven | Upper long strike - net debit ($510 - $3) |

Profit Zone | The range between both breakevens |

Iron Butterfly Example

The iron butterfly sells the at-the-money straddle and buys protection on both sides. It's a net credit trade, so you collect premium upfront rather than paying it. Still, the risk profile is like the long butterfly setup.

Leg | Strike | Action | Type |

|---|---|---|---|

Lower wing | $490 put | Buy 1 | Long put |

Short put | $500 put | Sell 1 | Short put |

Short call | $500 call | Sell 1 | Short call |

Upper wing | $510 call | Buy 1 | Long call |

Leg | Strike |

|---|---|

Lower wing | $490 put |

Short put | $500 put |

Short call | $500 call |

Upper wing | $510 call |

Leg | Action |

|---|---|

Lower wing | Buy 1 |

Short put | Sell 1 |

Short call | Sell 1 |

Upper wing | Buy 1 |

Leg | Type |

|---|---|

Lower wing | Long put |

Short put | Short put |

Short call | Short call |

Upper wing | Long call |

The premium collected from selling the straddle minus the premium paid for the wings (net credit) is how the max profit is calculated. Max loss is the wing width minus that credit. Breakevens land at the short strikes plus or minus the credit received. With the example above in mind, this trade might be routed for a $7.00 credit, with $3.00 max loss, and similar breakevens to the previous example.

Butterfly vs. Iron Condor: What's the Difference?

Both the butterfly and the iron condor are defined-risk strategies that profit from range-bound price action. The main difference is how wide the profit zone is.

Feature | Long Butterfly | Short Iron Condor |

|---|---|---|

Short strikes | 2 at the same strike | 2 at different strikes |

Profit zone | Narrow, peaks at one price | Wider range between short strikes |

Max profit | Only at the exact short strike | Anywhere between the two short strikes |

Net position | Debit or small credit | Net credit (typically) |

Best when | You have a precise price target | You expect a range, not a pinpoint |

Feature | Long Butterfly |

|---|---|

Short strikes | 2 at the same strike |

Profit zone | Narrow, peaks at one price |

Max profit | Only at the exact short strike |

Net position | Debit or small credit |

Best when | You have a precise price target |

Feature | Short Iron Condor |

|---|---|

Short strikes | 2 at different strikes |

Profit zone | Wider range between short strikes |

Max profit | Anywhere between the two short strikes |

Net position | Net credit (typically) |

Best when | You expect a range, not a pinpoint |

A butterfly concentrates max profit at a single price. An iron condor’s max profit spreads across a range. Butterflies have a lower probability of hitting max profit.

.png?format=png&auto=webp&quality=90&width=1000&disable=upscale)

When Butterfly Spreads Make Sense

The butterfly is a precise tool. It works best when you have a specific price target in mind and expect the underlying to stay there through expiration. A few situations where traders reach for it:

- Lower IV environments where a big move seems unlikely

- Post-earnings setups when the expected move looks priced in and the stock is likely to settle

- Underlyings with identified technical levels that could acting as magnets

- Situations where buying power is tight and you still want a defined-risk position with a good risk-reward ratio

Butterflies are theta-positive when the underlying is near the short strike. Time decay works in your favor when the underlying is sitting near the short strike. That makes the 21-30 DTE window particularly relevant, when theta starts accelerating.

The flip side: if the underlying makes a big directional move, the butterfly suffers. Any close outside the breakevens results in a partial or full loss of the net debit. The strategy does not recover from strong trending action.

Greeks at a Glance

Greek | Profile | What It Means In Practice |

|---|---|---|

Near-zero at entry (ATM body) | Direction-neutral at the start, but shifts as price moves away from the body | |

Positive (when the underling is near the short strike) | The position picks up value as time passes, as long as price is near the short strike | |

Negative | Rising IV typically hurts the trade; falling IV typically helps. This one catches traders off guard. | |

Position becomes increasingly sensitive to price movement near expiration | The position becomes more sensitive to price moves as expiration gets close |

Greek | Profile |

|---|---|

Near-zero at entry (ATM body) | |

Positive (when the underling is near the short strike) | |

Negative | |

Position becomes increasingly sensitive to price movement near expiration |

Greek | What It Means In Practice |

|---|---|

Direction-neutral at the start, but shifts as price moves away from the body | |

The position picks up value as time passes, as long as price is near the short strike | |

Rising IV typically hurts the trade; falling IV typically helps. This one catches traders off guard. | |

The position becomes more sensitive to price moves as expiration gets close |

Negative vega is worth examining. Even when the underlying sits right at your target, a spike in implied volatility can erode the position's value due to extrinsic value increasing in the strikes. That's why butterflies tend to work better in lower IV environments, where there's less risk of IV expansion undoing your thesis while you wait.

Managing the Trade

How you manage a butterfly depends on whether it's a debit or credit structure and where the underlying is trading relative to your target.

For debit butterflies, most traders don't hold through expiration. Taking profits at 25-50% of max profit is a common approach, because in the final days, the payoff curve gets choppy and pin risk becomes a real factor near the short strikes.

When the underlying moves away from your strike, the position loses value quickly. At that point, many traders cut the loss and move on rather than waiting for the underlying to come back. Some hold since risk is defined. Time is not on your side once you're outside the profit zone.

Pin risk deserves attention. If the underlying closes right at the short strike on expiration day, it's unclear whether those body options will be assigned. That can leave you with an unexpected overnight position with undefined risk. Closing the butterfly before expiration sidesteps this entirely.

Frequently Asked Questions

A butterfly spread is a defined-risk options strategy that uses three strike prices. You buy one contract at a lower strike, sell two at a middle strike, and buy one at an upper strike. The trade profits when the underlying closes near the middle strike at expiration. Max profit and max loss are both defined at entry.

For a long call or put butterfly, max profit is the lower wing width minus the net debit paid, multiplied by 100 for equity options. You only hit that maximum if the underlying closes exactly at the short strike at expiration. For an iron butterfly, max profit is the net credit received, achieved when the underlying pins the short strikes at expiration, and all legs expire worthless.

The butterfly loses money when the underlying moves far enough away from the short strike that the position closes outside the breakevens. The maximum loss on a debit butterfly is the net debit paid. For an iron butterfly, max loss is the wing width minus the credit received. Both worst-case scenarios happen when the underlying closes at or beyond either outer strike.

A vertical spread uses two strikes and profits from directional price movement. A butterfly uses three strikes and profits from the underlying staying near one price. Butterflies can be direction-neutral at entry; verticals carry a directional lean. The tradeoff: butterflies have a narrower profit zone but can offer stronger risk-reward ratios when the underlying lands exactly where you want it.

Defined-risk strategies including butterfly spreads are generally available in IRA accounts on tastytrade, subject to the account's trading permissions. The capital required is the net debit for a debit butterfly. Review your account permissions or contact tastytrade support to confirm eligibility.

Options involve risk and are not suitable for all investors as the special risks inherent to options trading may expose investors to potentially significant losses. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

All investments involve risk of loss. Please carefully consider the risks associated with your investments and if such trading is suitable for you before deciding to trade certain products or strategies. You are solely responsible for making your investment and trading decisions and for evaluating the risks associated with your investments.

Multi-leg option strategies incur higher transaction costs as they involve multiple commission charges.