The iron condor is a defined-risk, four-leg options strategy that profits from neutral price action and time decay. It combines a short call spread and a short put spread collected as a net credit. This article covers construction, profit & loss mechanics, breakevens, management, and frequently asked questions.

The iron condor is a defined-risk, four-leg options strategy that profits when an underlying asset stays within a specific price range through expiration. It is constructed by selling an out-of-the-money (OTM) call spread and an OTM put spread in the same expiration cycle, collecting a net credit.

What Is an Iron Condor?

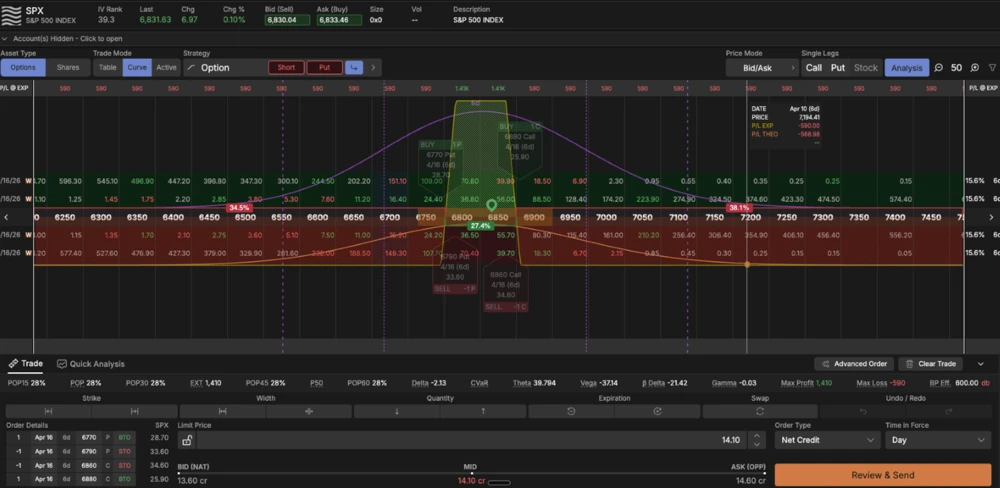

An iron condor consists of four options: a short OTM call, a long OTM call at a higher strike, a short OTM put, and a long OTM put at a lower strike, all in the same expiration. The short call spread caps upside risk. The short put spread caps downside risk. The net credit collected at entry is the maximum profit on the position.

The position profits when the underlying stays between the two short strikes through expiration. Both spreads expire worthless, and the trader keeps the full credit. Time decay (theta) works in favor of the position each day the underlying remains within the profit range.

Max loss occurs when one of the spreads expires fully in-the-money (ITM), which is the width of the ITM spread less the credit received.

Iron Condor Construction

Every iron condor has two spread components:

Short call vertical spread (bearish side)

- Sell an OTM call at a higher strike than the current price

- Buy a further OTM call to cap upside risk

Short put vertical spread (bullish side)

- Sell an OTM put at a lower strike than the current price

- Buy a further OTM put to cap downside risk

Both spreads share the same expiration. The distance between the short and long strikes on each side is the spread width. Both spreads are typically the same width, though they do not have to be. The trade opens for a net credit, which is the sum of both spread credits.

tastytrade displays the probability of profit (POP) natively on every position, making it straightforward to evaluate the statistical likelihood of a given setup at a glance. Probability of profit is a mathematical estimate based on the options market's pricing at a given moment and does not guarantee any outcome.

Iron Condor Example

The following is a hypothetical illustration of mathematical principles. It does not predict or project the performance of any investment or investment strategy and is not a recommendation to buy or sell any security.

TSTY is trading at $175.

Leg | Strike | Action | Premium |

|---|---|---|---|

Short call | 190 | Sell | +$2.00 |

Long call | 195 | Buy | −$0.50 |

Short put | 160 | Sell | +$2.25 |

Long put | 155 | Buy | −$0.75 |

Leg | Strike |

|---|---|

Short call | 190 |

Long call | 195 |

Short put | 160 |

Long put | 155 |

Leg | Action |

|---|---|

Short call | Sell |

Long call | Buy |

Short put | Sell |

Long put | Buy |

Leg | Premium |

|---|---|

Short call | +$2.00 |

Long call | −$0.50 |

Short put | +$2.25 |

Long put | −$0.75 |

Call spread credit: $1.50 ($150)

Put spread credit: $1.50 ($150)

Total credit collected: $3.00 ($300)

Factor | Calculation | Result |

|---|---|---|

Max Profit | Total credit collected | $300 |

Max Loss (call side) | (Spread width − total credit) × 100 | ($5.00 − $3.00) × 100 = −$200 |

Max Loss (put side) | (Spread width − total credit) × 100 | ($5.00 − $3.00) × 100 = −$200 |

Upside Breakeven | Short call strike + total credit | $190 + $3.00 = $193 |

Downside Breakeven | Short put strike − total credit | $160 − $3.00 = $157 |

Factor | Calculation |

|---|---|

Max Profit | Total credit collected |

Max Loss (call side) | (Spread width − total credit) × 100 |

Max Loss (put side) | (Spread width − total credit) × 100 |

Upside Breakeven | Short call strike + total credit |

Downside Breakeven | Short put strike − total credit |

Factor | Result |

|---|---|

Max Profit | $300 |

Max Loss (call side) | ($5.00 − $3.00) × 100 = −$200 |

Max Loss (put side) | ($5.00 − $3.00) × 100 = −$200 |

Upside Breakeven | $190 + $3.00 = $193 |

Downside Breakeven | $160 − $3.00 = $157 |

When the spreads have different widths, max loss is calculated using the wider spread. The long options on each side cap the loss at a defined amount. This is what makes the iron condor a defined-risk strategy.

Multi-leg option strategies incur higher transaction costs as they involve multiple commission charges. See tastytrade pricing and fees for a full breakdown.

Iron Condor Profit and Loss

Maximum profit equals the total net credit received at entry. It is achieved when both spreads expire OTM and all four options settle at zero. The full credit is retained.

Maximum loss equals the width of the wider spread minus the total credit collected. The loss is the same whether the underlying moves through the call side or the put side assuming both sides have the same spread width. Whichever spread is fully in the money at expiration produces the max loss scenario. The position cannot lose more than this defined amount if one of the spreads expires ITM.

Breakevens at expiration:

- Upside: Short call strike + total credit received

- Downside: Short put strike − total credit received

Prior to expiration, the position can be closed for a profit if the condor can be purchased for a debit less than the original credit. Closing early removes all remaining risk, including the risk of the underlying reversing back through the profit zone before expiration.

When Traders Use Iron Condors

The iron condor is a directionally neutral strategy. It is not suitable for all traders or all market environments. Traders who use it typically do so when:

- Implied volatility (IV) is higher than their individual outlook for the stock

- They expect the underlying to trade sideways or stay within a defined range for a period of time

The iron condor's defined-risk profile also makes it available for IRA accounts at tastytrade, where undefined-risk short options positions are not permitted.

Traders should carefully evaluate whether this strategy is appropriate for their individual investment profile, risk tolerance, and objectives before placing any trade.

Greeks Profile

The iron condor has a distinct Greek profile that drives the mechanics of the position:

Theta (time decay): Positive. The position gains value each day, all things being equal, as the options decay toward zero. Time decay is the primary source of profit in the iron condor.

Delta: Near zero at initiation when the short strikes are placed equidistant from the current price. The position develops directional exposure if the underlying moves toward one of the short strikes.

Vega: Negative. The position loses value when implied volatility expands and gains when IV contracts. This is why many traders prefer entering condors in higher-IV environments, where a subsequent contraction in IV can accelerate the decay of both spreads.

Gamma: Negative. Short gamma means losses accelerate when the underlying makes a sharp move in either direction. Gamma risk is highest in the days immediately before expiration.

Managing an Iron Condor

Position management decisions depend on individual risk tolerance, account size, and objectives. The approaches below are illustrative of common techniques and are not recommendations.

Closing for a profit target. One common approach is placing a good-till-canceled (GTC) order to close the position at a specific profit threshold. For example, when the condor can be purchased for 50% of the original credit. A $3.00 credit condor would be closed at a $1.50 debit under this approach. Closing early eliminates all remaining risk in exchange for forgoing the remaining potential profit.

Managing the untested side. When the underlying moves toward one short strike, the opposite spread (the untested side) has often decayed significantly and may have little remaining value. Closing the untested side for a small debit reduces the net risk of the remaining position to a single short spread.

Rolling a threatened spread. If the underlying approaches a short strike before expiration, the at-risk spread can be rolled to a further OTM strike in the same or a later expiration. Rolling can collect additional credit and can move the short strike away from the current price, but it extends the duration of the trade and increases buying power usage.

Closing at a loss. If the underlying moves through a short strike and the spread moves deep ITM, closing the full position limits the realized loss to something below the maximum. Remaining in the position risks a loss up to the defined maximum at expiration. Traders often pre-define a loss threshold before entering the trade.

Expiration Risk

A defined-risk spread is only defined risk if both legs settle the same way at expiration. The risk specific to expiration is called assignment risk: the short strike finishes in the money while the long strike finishes out of the money, leaving the short option subject to automatic exercise with no offsetting long option.

Options that expire in the money by $0.01 or more are automatically exercised by the OCC. If the short put expires ITM, it is assigned and converts to 100 long shares of stock per contract. If the short call expires ITM, it converts to 100 short shares. In either case, the position is no longer flat. It carries overnight directional stock risk into the next trading session.

After-hours risk also applies. An option that appeared to be OTM at the 4:00 p.m. ET closing print can become ITM based on after-hours price movement. The standard OCC exercise deadline is 5:30 p.m. ET. A sharp post-close move can result in an unexpected assignment even after the regular session close.

The only way to eliminate both pin risk and assignment risk is to close the position before expiration.

Iron Condor vs. Related Strategies

The iron condor belongs to a family of defined-risk premium-selling structures. The differences between related strategies involve the trade-off between credit collected and range of profitability.

Short strangle. A strangle sells a naked OTM call and OTM put with no long-option protection. It collects more credit and benefits from a wider range of profitability compared to the condor, but it is an undefined-risk position. The iron condor adds long wings to cap maximum loss. The trade-off is a smaller credit in exchange for defined risk.

Iron butterfly. An iron butterfly sells the call and put at the same at-the-money strike rather than at separate OTM strikes. It collects a larger credit but has a much narrower max profit range — essentially requiring the underlying to close very near a single price at expiration. The iron condor accepts a smaller credit in exchange for a wider max profit zone between the two short strikes.

Short call spread / short put spread. Each vertical spread is one half of an iron condor. Traders with a moderately directional view may prefer a single spread. The iron condor combines both for a fully neutral position.

Iron Condor on Index Options

Index options are used by experienced traders for several structural reasons worth understanding:

Section 1256 tax treatment. Index options that qualify as Section 1256 contracts receive blended capital gains treatment. 60% long-term and 40% short-term, regardless of the holding period. Traders should consult a qualified tax professional regarding their individual tax situation. tastytrade does not provide tax advice.

Cash settlement. Index options settle in cash rather than in shares. This means a short option that expires in the money results in a cash debit or credit rather than a stock position. Cash settlement eliminates the risk scenario of a spread converting into shares at expiration.

Frequently Asked Questions

The maximum profit on an iron condor equals the total net credit received when the position was opened. It is achieved when all four options expire out of the money and worthless. The full credit is retained. Max profit is only realized if the underlying closes between the two short strikes at expiration.

Maximum loss equals the width of the wider spread minus the total net credit received. For example, a $5-wide condor opened for a $3.00 credit has a maximum loss of $2.00 per share, or $200 per contract. The long options on each side cap the loss. The position cannot lose more than this defined amount regardless of how far the underlying moves if a spread expires fully ITM.

There are two breakeven prices at expiration. The upside breakeven equals the short call strike plus the total credit received. The downside breakeven equals the short put strike minus the total credit received. The position is profitable at expiration if the underlying closes between these two prices. Breakeven calculations apply at expiration only; prior to expiration, the position value is affected by implied volatility, time remaining, and the underlying price.

There is no universal answer. The decision depends on individual risk tolerance, account objectives, and how the position has moved. Some traders set a profit target at a percentage of the original credit and use a GTC order to close automatically when that level is reached. Others close when a loss threshold is exceeded. Closing early removes all remaining risk and eliminates exposure to expiration risk.

Iron condors are available in IRAs at tastytrade because both spreads are defined-risk structures. The iron condor's long wings on each side define the maximum loss, qualifying it for IRA trading permissions at tastytrade. Account approval is required and not guaranteed.

If the short put expires in the money, it is automatically exercised and converts to 100 long shares of stock per contract. If the short call expires in the money, it converts to 100 short shares. If the corresponding long option also expires in the money, it offsets the assignment. If only the short option expires in the money (assignment risk), the position carries unhedged stock risk overnight. Closing the position before expiration is the only way to eliminate this risk.

Options involve risk and are not suitable for all investors as the special risks inherent to options trading may expose investors to potentially significant losses. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

All investments involve risk of loss. Please carefully consider the risks associated with your investments and if such trading is suitable for you before deciding to trade certain products or strategies. You are solely responsible for making your investment and trading decisions and for evaluating the risks associated with your investments.

Multi-leg option strategies incur higher transaction costs as they involve multiple commission charges.