Long Put Vertical Spread Options Strategy Explained

Contents

Long Put Vertical Summary

- A long put vertical spread is a bearish position involving a long and short put with different strike prices in the same expiration.

- When setting up a put debit spread, the long put is more expensive than the short put since it is closer to the money, resulting in a net debit.

- Selling a put at a lower strike price against the long put can reduce the overall cost of establishing a bearish position, but it also caps the downside profit potential.

- Max profit occurs when the entire spread expires ITM and is calculated by subtracting the debit paid from the long put spread width.

- The debit paid for the long put vertical spread is an investor's max loss if it expires OTM and is worthless at expiration. However, the underlying can expire in between the spread, resulting in 100 short shares (per contract) from the long put auto-exercising for being ITM. Short shares have unlimited risk; as always, manage your positions according to your plans.

Long Put Vertical Spread

A long put vertical spread is a bearish strategy where the trader wants the underlying price to fall. A long put vertical consists of two put options in the same expiration: a long put closer to the stock price and a short put further out-of-the-money (OTM) than the long put. When setting up a put debit spread, the long put is worth more than the short put, resulting in a net debit when establishing. Selling a put at a lower strike price against the long put reduces the overall cost of establishing a bearish position and is generally cheaper than buying a single put option outright. However, by selling a put against it, downside profit potential is capped.

The value of a long put vertical spread can appreciate as the price of the stock or ETF drops and approaches the long strike price and, ideally, past the short put’s strike price. The ideal scenario is when the stock price drops below the short put strike at expiration so it can appreciate to its maximum value, which is its spread width.

Conversely, the value of the long put vertical spread can depreciate when the price of the underlying it tracks rises. Additionally, due to time decay, the value of the spread can depreciate over time if the underlying price remains constant and does not approach or drop below the long put's strike price.

Unlike buying a single put option outright, a long put vertical spread allows you to reduce your overall cost to deploy the bearish strategy. Due to the lowered cost, the max loss is less than buying the put outright. However, the max profit of the strategy is capped because of selling a further out-of-the-money put against the long put.

Investors can close or sell the long put spread for a higher amount than what the trader paid for it to book a profit before expiration or sold for less than the debit paid up front to minimize the max loss. In other words, the trade does not have to be held to expiration to yield a profit or loss potentially.

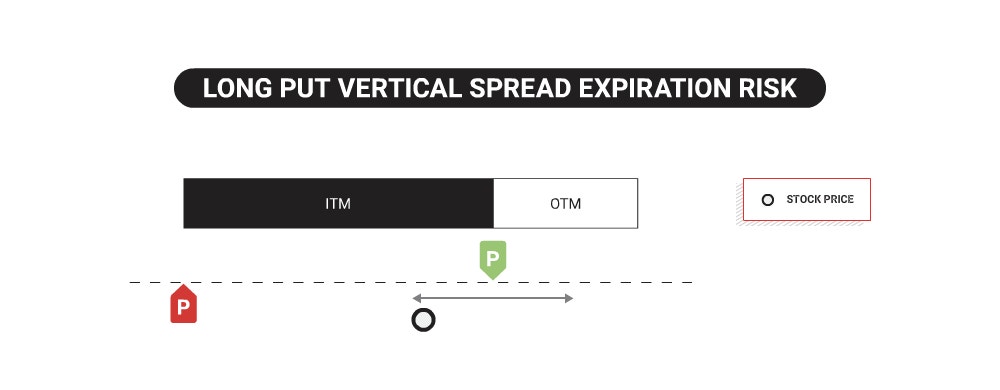

Expiration Risk for Long Put Vertical Spreads

A defined-risk vertical spread is no longer a defined risk position if one leg of the spread expires in the money and the other does not. The risk lies with pin risk on the day of expiration, which is the risk surrounding the uncertainty of where the underlying will close to determine whether an option is in or out of the money. Options that expire in the money by $0.01 or more are auto-exercised, resulting in the long put option converting to 100 short shares of stock. In the case of a long put vertical spread, a partially ITM spread will convert to 100 short shares, and the OTM short put option would not get assigned to offset the short shares [with long shares]. When you end up with short shares, the risk is unlimited to the upside, so manage accordingly.

Additionally, any options strategy involving short options, including a long put vertical, may face after-hours risk on the day of expiration. In summary, although the vertical may have expired OTM based on the stock's closing print, an OTM short put option can become ITM based on any extreme downward price movement after the market close, resulting in an unexpected assignment of long shares. As a result, the investor would assume the risk of 100 long shares per contract assigned. The only way to eliminate after-hours risk is by closing any short options positions before expiration.

Due to the risk of exercise and assignment, it's crucial to have a plan and manage risk like closing or rolling the position before expiration, especially when the account does not have sufficient account equity to take on the resulting position. Please visit the tastytrade Help Center to learn more about Expiration Risk.

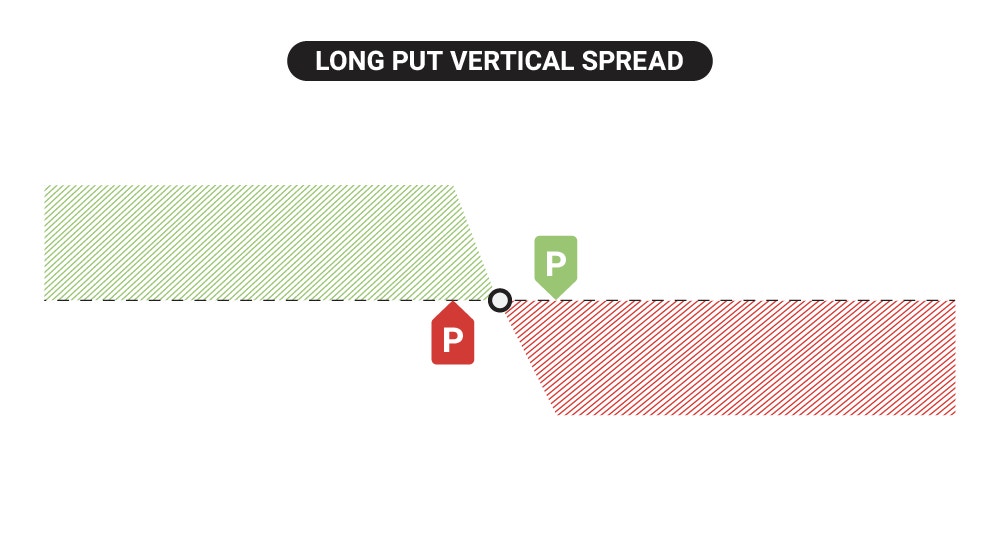

Profit & Loss Diagram of a Long Put Vertical Spread

A long put vertical spread can become profitable if the underlying approaches the long put’s strike price or surpasses it by the amount of the debit paid for the entire spread. Unlike outright long puts, the profit of the long put vertical spread caps if the underlying price breaches the short put strike at expiration, which the flattened green area below illustrates.

Losses on the long put spread can occur if the underlying remains constant and does not approach the long put’s strike price or does not surpass the breakeven point at expiration, as shown where the P/L line converges with the x-axis. The maximum loss on a long put vertical is only the net debit paid, which the flattened red area of the diagram illustrates, and occurs when the spread expires out-of-the-money and worthless.

What’s Required for a Long Put Vertical Spread?

Two put options in the same expiration.

- Buy to Open +1 long put

- Sell to Open -1 short put (any strike price below the long put)

Example of a Vertical Put Debit Spread

XYZ currently trading @ $55

- +1 XYZ 50-strike put @ $3 debit

- -1 XYZ 45-strike put @ $1.50 credit

Paid a $1.50 debit ($150 total)

Spread Width: Long put strike – Short put strike = 50 – 45 = $5

Time Decay Affect | Works against the option’s value |

Max Profit | (Spread width) x 100 – Total debit paid (50 - 45) x 100 – ($1.50 x 100)= $350 |

Max Loss | Total debit paid $150 |

Breakeven Price (at expiration) | Long Strike price - Debit paid $50 - $1.50 = $48.50 |

Buying Power Requirement | Debit paid $150 |

Account Type Required | Margin and IRA |

Other Names | Bear put spread Put debit spread Long put spread Long put vertical |

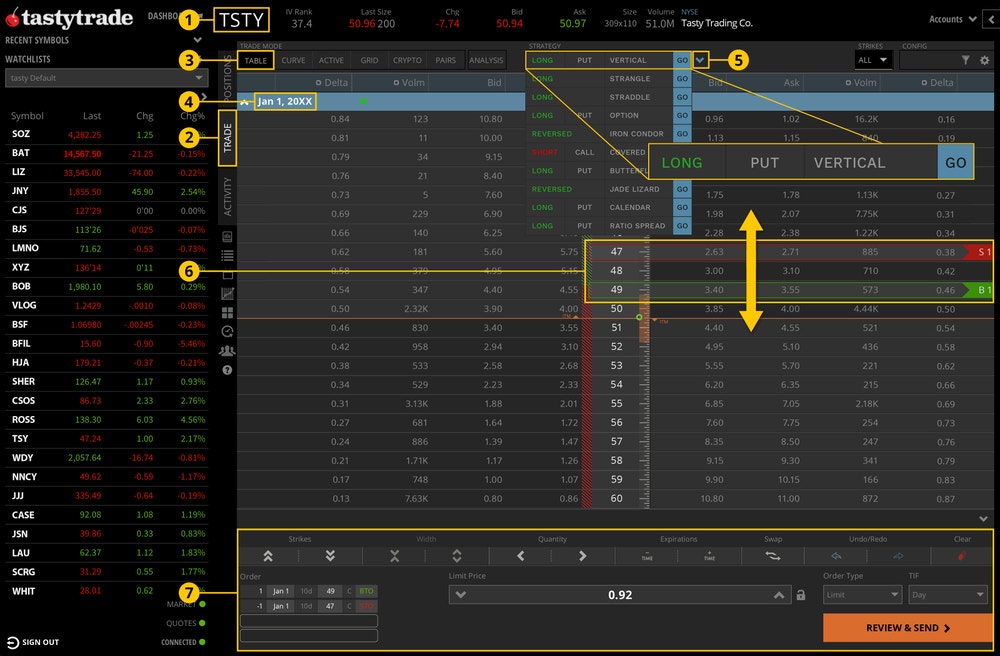

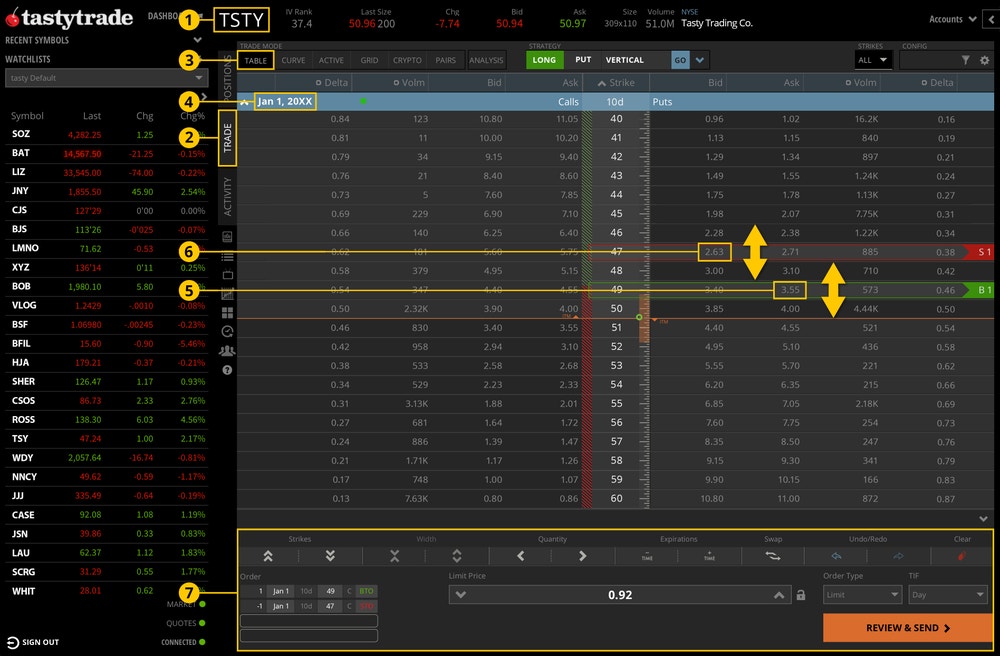

How to place a put vertical debit spread order on the tastytrade desktop platform

Using the Strategy Menu

- Enter a symbol.

- Navigate to the Trade tab.

- Go to the Table mode.

- Click on an expiration date to expand.

- Click the Strategy Menu and locate the Vertical strategy. From left to right, click each column to display Long, Put, and Go.

- The long strike order will display a green bar, and the short strike will display in a red bar in the expanded expiration. Drag each strike up or down to the desired strike.

- Go to the order ticket to determine the quantity, price, time-in-force (TIF), etc. before clicking "Review & Send." Review everything including commissions and fees before sending the order.

Building it Manually

- Enter a symbol.

- Navigate to the Trade tab.

- Go to the Table mode.

- Click on an expiration date to expand.

- Click the Ask price of the long leg.

- Click the Bid price of the short leg.

- Go to the order ticket to determine the quantity, price, time-in-force (TIF), etc. before clicking "Review & Send." Review everything including commissions and fees before sending the order.

All investments involve risk of loss. Please carefully consider the risks associated with your investments and if such trading is suitable for you before deciding to trade certain products or strategies. You are solely responsible for making your investment and trading decisions and for evaluating the risks associated with your investments.

Multi-leg option strategies incur higher transaction costs as they involve multiple commission charges.

Options involve risk and are not suitable for all investors as the special risks inherent to options trading may expose investors to potentially significant losses. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.